Goodwill is one of the types of intangible

assets that appears as a result of a business combination across different companies. The recognition and accounting for goodwill is set out in IFRS 3 Business Combinations.

The amount of goodwill, in accordance with international financial reporting standards, is reflected in the company’s statement of financial position as part of its non-current assets.

Examples of cases in which an entity needs to calculate and report goodwill include the purchase or sale of a business and mergers and acquisitions.

Goodwill is generally calculated as the difference between the total cost of the acquisition and the net assets acquired, less

liabilities assumed. Assets and liabilities are measured at a fair value. It should be noted that under

IFRS, goodwill is recognized and reported at the acquisition date.

Goodwill can also be negative. For such cases, such a concept as a bargain purchase is used, and in this situation, goodwill is reflected not as a balance sheet indicator but as one of the types of

income of the organization in the profit and loss statement. However, in practice, such situations are considered rare because business owners most often do not sell the company at a price below fair value.

For example, in 2021, the goodwill of the German company

Volkswagen, according to its financial statements, amounted to EUR 26.174 billion. Together with goodwill, the organization’s intangible assets amounted to EUR 77.689 billion. One of the transactions was the acquisition of

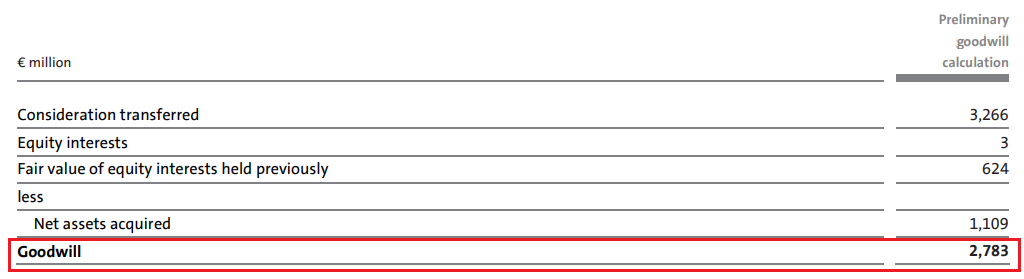

Navistar International by its subsidiary

Traton Group. This transaction resulted in goodwill of EUR 2.783 billion.

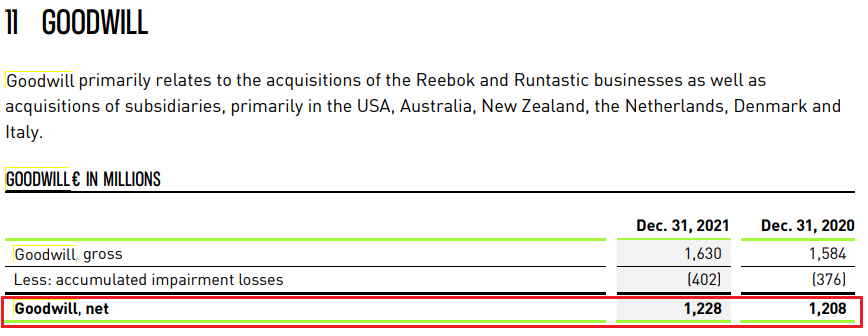

Another example is

Adidas, which had EUR 1.228 billion in goodwill as of December 31, 2021.

RAS

RAS uses the term “business reputation” instead of goodwill, which is calculated in a similar way. At the same time, a positive business reputation is considered a premium to the price paid by the buyer, and a negative reputation, on the contrary, is considered a discount.

Goodwill acquired is amortized over 20 years. The depreciation period should not exceed the life of the company itself. The procedure for accounting for goodwill is prescribed in PBU 14/2007, “Accounting for intangible assets”.